New Land Loan products introduced are :

· NRP(commercial) plot Loan

· Refinance(BT) Plot Loan

· Refinance(BT) NRP Plot Loan

· Refinance(BT) NRI Plot Loan

Key features of the new policy are :

IIR/FOIR (Instalment to Income ratio/fixed obligation to Instalment ratio):

Double Whammy Score( DW):

o Direct allotment: (LCR + IIR/FOIR=115)

o Resale: (LTV + IIR/FOIR=115)

(LTV has to be considered while calculating DW instead of LCR)

Fee for land loans

Simultaneous financing of plot purchase and construction

These applications are to be considered as normal housing loan applications and fees, rates and LCR norms will be as applicable to housing loans. However in such cases the first disbursement of the loan should not exceed the plot cost minus the own contribution. Subsequent to part disbursement, the customer may defer construction plans and want to commence repayment on the amount disbursed towards plot purchase. Loan utilization having been towards plot purchase, the product is to be changed to that of a plot purchase loan and rates applicable to Plot Purchase loans will be applicable.

Financing of plot purchase to be subsequently followed by a request to finance construction on the same plot

If the customer approaches us for a loan for construction after some time, the process to be followed will involve the customer making a new housing loan application (for construction plus adjustment of the outstanding plot purchase loan). Part of this loan will be utilised for prepayment of the outstanding plot purchase loan through an internal adjustment at the time of disbursement. This new combined loan will be sanctioned as a housing loan. The maximum loan will be plot loan outstanding plus 80%/85% of construction cost. Incase of a reduction in the value of plot care should be taken to ensure that the LCR of the construction component is capped at a level where the current market value of plot and construction is within acceptable limits. Fees as applicable to be collected only on the additional loan.

· NRP(commercial) plot Loan

· Refinance(BT) Plot Loan

· Refinance(BT) NRP Plot Loan

· Refinance(BT) NRI Plot Loan

Key features of the new policy are :

- This will be applicable to all new & under process applications w.e.f. from 1st January 2013.

- Max no of live plot loans have been restricted to 2 (including new plot loan application) that can be availed by a customer at a time.

- Plot loan availed (in the capacity of borrower/co-borrower) even from other institution and outstanding on the date of approval will be included in the above criteria. However loans prepaid/repaid will not be considered in above criteria.

- Loans availed by spouse will NOT be included in the above criteria.

- Loans for commercial plots (NRP LAND) can also be considered

- Minimum size of the plot should 100 sqm.

- Projects with plot sizes less than 100 sqm can be considered purely as an exception depending on location and value and with approval from the branch manager.

- Undertaking from customer/s to be taken that he would commence construction on the plot for which loan is availed within a period of 5 yrs from the date of first disbursement. In the event of non compliance of above. HDFC reserve the right to increase the rate of interest. (Drafts of indemnity to be used for Builder cases and Authority cases enclosed)

- All cost payable by customer in cheque to developer should be included except stamp duty & registration charges

IIR/FOIR (Instalment to Income ratio/fixed obligation to Instalment ratio):

- Maximum IIR/FOIR that can be extended is 50% keeping in mind the profile of customer/s and their cash flow.

- The maximum term that can be extended is 180 months or the retirement age whichever is lower

Double Whammy Score( DW):

- This has now been revised to 115 as detailed below:

o Direct allotment: (LCR + IIR/FOIR=115)

o Resale: (LTV + IIR/FOIR=115)

(LTV has to be considered while calculating DW instead of LCR)

Fee for land loans

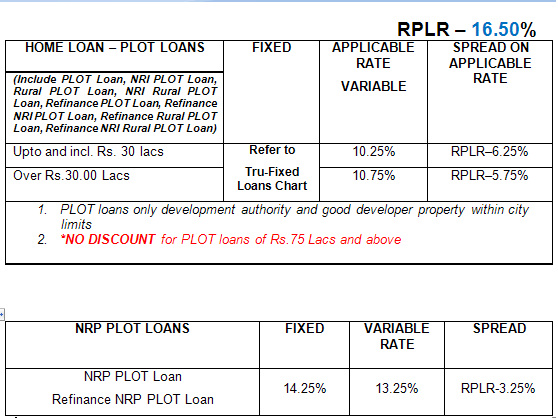

- Residential plot loan - as applicable on home loans

- NRP plot loan - as applicable on NRP loans

Simultaneous financing of plot purchase and construction

These applications are to be considered as normal housing loan applications and fees, rates and LCR norms will be as applicable to housing loans. However in such cases the first disbursement of the loan should not exceed the plot cost minus the own contribution. Subsequent to part disbursement, the customer may defer construction plans and want to commence repayment on the amount disbursed towards plot purchase. Loan utilization having been towards plot purchase, the product is to be changed to that of a plot purchase loan and rates applicable to Plot Purchase loans will be applicable.

Financing of plot purchase to be subsequently followed by a request to finance construction on the same plot

If the customer approaches us for a loan for construction after some time, the process to be followed will involve the customer making a new housing loan application (for construction plus adjustment of the outstanding plot purchase loan). Part of this loan will be utilised for prepayment of the outstanding plot purchase loan through an internal adjustment at the time of disbursement. This new combined loan will be sanctioned as a housing loan. The maximum loan will be plot loan outstanding plus 80%/85% of construction cost. Incase of a reduction in the value of plot care should be taken to ensure that the LCR of the construction component is capped at a level where the current market value of plot and construction is within acceptable limits. Fees as applicable to be collected only on the additional loan.

ROI on plot loan

RSS Feed

RSS Feed